AI and cybersecurity to drive CEE tech sector

1 hour ago

Executive Summary

The second wave of the coronavirus (COVID-19) pandemic appears not to have affected Kazakhstan to the same extent that it has certain other nations. Kazakhstan currently has no plans to implement a third nationwide lockdown and has been focusing on applying regionalised restrictions instead. Kazakh Health Minister Alexey Tsoy has alluded to the possibility of a lockdown in the commercial capital, Almaty, in mid-January 2021. The country’s second national lockdown in July-August was not as strict as those of other nations. As the government fears crippling the retail sector, any new lockdowns may follow a similar model.

The January 2021 parliamentary elections will almost certainly maintain the existing balance of power, with the ruling Nur Otan (Radiant Fatherland) political party, controlled by former president of three decades Nursultan Nazarbayev, set to retain control over the lower house of parliament (Majilis).

International observers expect Kazakhstan’s economy to rebound to growth of somewhere between 3.5%-4.5% y/y in 2021.

“Despite elevated deficits, the reserve buffers should remain high, as [the National Fund’s] FX assets are likely to fall from 35% of GDP in 2019 to 30% of GDP by YE21,” London-based broker Sova Capital projected in a note in December.

A general weakening of inflationary pressures is also expected in 2021 along with a recovery of the Kazakh national currency. That would be thanks to a rebound in world oil prices as part of the global recovery from the pandemic.

The Kazakh banking sector’s consolidation might continue in 2021, following the trajectory set in the previous few years.

The government’s plans for initial public offerings (IPOs) of major state-run companies on the London Stock Exchange (LSE) are likely to suffer further delays as the markets would not necessarily provide an advantageous course for the flotations despite the anticipated pick-up in the global economy.

Political Outlook

- Elections

The government has scheduled the parliamentary election for January 10. The day will mark the country’s first such poll since Kassym-Jomart Tokayev succeeded Nursultan Nazarbayev, who resigned in 2019. Nazarbayev still maintains a grip on power via the Nur Otan party and the country’s Security Council. The 107-seat Majilis is dominated by 84 Nur Otan lawmakers. The pro-government Communist People’s Party of Kazakhstan and the liberal Ak-Zhol party each hold seven seats. Nine are filled by a Nazarbayev-controlled advisory body.

Six registered political parties were originally meant to take part in the election, namely Nur Otan, four pro-government parties (Aq Zhol, Auyl, Birlik and the Communist People's Party) and the All-National Social Democratic Party of Kazakhstan (OSDP). However, the OSDP, which officially labels itself as an opposition group, announced on November 27 that it would boycott the election. Its leader Askhat Rakhimzhanov said the decision was based on the ex-Soviet state’s political scene continuously being dominated by the “same” political elite.

Prior to the OSDP’s announcement, Kazakh fugitive banker and dissident, Mukhtar Ablyazov, called on his supporters in a November 17 video posted on Facebook to join and vote for the OSDP to "prove" the party is a "fraud."

The results of the parliamentary vote are a foregone conclusion and can be seen as rigged in favour of Nur-Otan. Barring any major protests driven by growing economic anxieties amid the pandemic, the elections will most probably go smoothly for the ruling elite. Kazakhstan has not shown any precedent for a major organised protest movement like in Belarus and has no conditions set for Kyrgyzstan-style inter-elite squabbles.

The only potential for widespread protests might echo from 2019’s countrywide demonstrations seen during the snap election to replace long-time ruler Nazarbayev with his handpicked shoo-in successor Tokayev. The difference between the snap presidential election and the parliamentary vote, however, is that the former provided a clear opposition candidate to rally behind. The Kazakh population currently finds itself in survival mode, demorilised by the pandemic and the global recession. It is thus less likely to resort to any kind of political action.

The authorities appear to be cautious, nonetheless. This can be seen in the government’s recent targeting of human rights organisations.

- Human rights

Amnesty International, Front Line Defenders, Human Rights Watch (HRW) and International Partnership for Human Rights said in a joint statement in December that the Kazakh tax authorities since mid-October have notified at least 13 human rights groups in the country of what they claimed were incorrectly completed foreign income declaration forms.

Failure to fill out the forms in a timely manner carries a fine of around $1,300 in local currency-equivalent and a suspension of activities followed by a greater fine and a ban on activities for a repeat offence carried out within the same year. The notified groups include the Kazakhstan International Bureau for Human Rights and Rule of Law; the International Legal Initiative; Qadyr Qasiyet; and Echo Public Foundation. The groups work on issues ranging from environmental rights and election monitoring to media freedom and freedom of expression.

The international human rights organisations called on the Kazakh authorities to "immediately drop these unfounded complaints against independent civil society organizations and live up to their international human rights obligations to respect, protect, promote, and fulfill human rights, including the right to freedom of association."

“Targeting over a dozen prominent human rights groups with alleged financial reporting violations is more than gross overreach by Kazakhstan tax authorities,” said Marie Struthers, Eastern Europe and Central Asia director at Amnesty International. "It is a cynical attempt to silence independent and critical voices precisely when these voices matter the most.”

“It is of particular concern that the increased targeting coincides with the upcoming parliamentary election in January 2021,” said Andrew Anderson, executive director at Front Line Defenders.

The row does not look good when it comes to Kazakhstan’s international standing. Shortly before it occurred, the UN Working Group on Arbitrary Detention in November 2020 came to the conclusion that the Kazakh government violated international human rights law in 2019 by detaining activist Serikzhan Bilash. Further targeting human rights activism on top of this might only exacerbate Kazakhstan’s difficulties in avoiding the image of a dictatorial regime potentially set to slide into deeper authoritarianism in 2021.

This potential can especially be observed in Kazakh President Kassym-Jomart Tokayev’s reforms on public protests that demand strictly controlled peaceful assemblies with a defined number of people that can attend, determine the availability of venues for rallies and demand that organisers of public protests obtain a specified permit. The reforms are meant to suggest an expansion of freedoms, but critics have said that the reform law falls short of international human rights standards.

“Despite some changes in procedures, the law leaves room for Kazakhstan’s authorities to continue to unjustifiably restrict people from exercising their right to peaceful protest,” said Mira Rittman, an HRW researcher for Europe and Central Asia.

This trend can also be observed in the government’s repeated efforts at the end of 2020 to set further restrictions on internet freedom.

- Internet freedom

In December, the government temporarily forced citizens in the capital Nur-Sultan to install digital root certificates on devices. The citizens were denied access to foreign internet services if they failed to accept the installation.

The move marks the third attempt by the authorities to force the installation of root certificates. There was a first attempt in December 2015 and a second attempt in July 2019. If installed, the certificate allows the government to intercept all HTTPS traffic generated by the monitored citizens’ devices via a technique called MitM (Man-in-the-Middle). Both previous attempts failed due to browser makers blacklisting the government's certificates.

A statement published on December 4 by the authorities claimed that the efforts to intercept HTTPS traffic were a cybersecurity training exercise for government agencies, telecoms and private companies. A similar “training exercise” was undertaken around the time of the countrywide rallies seen during the snap presidential vote in 2019.

International watchdog Freedom House has labelled Kazakhstan as "Not Free" with a Global Freedom Score of 23 out of 100. It has also tagged it as a "Consolidated Authoritarian Regime" with a Democracy Percentage of 5 out 100 and a Democracy Score of 1.32 out of 7.

Macro Economy

- GDP

The oil export-reliant Kazakh economy has felt the effects of the pandemic-driven drop in energy prices along with the disruption in its service sector caused by two national lockdowns and quarantine restrictions.

Kazakhstan’s GDP contracted 2.8% y/y in the first nine months of 2020, according to latest figures published by the Statistical Committee of Kazakhstan. The contraction was driven by a decline in the services sector, which was hit by the lockdowns brought in to stem the spread of the coronavirus in March-May and July-August. The economy was also affected by global impacts of the pandemic, including, it bears repeating given how important oil remains to Kazakh economic health, falling demand for energy and reduced world oil prices. The service sector accounted for 53.3% of total GDP in the nine-month period, while industry accounted for 29.2%.

Kazakhstan's short-term economic indicator, a narrower gauge of annual GDP growth, constituting 60% of Kazakh GDP, continued to contract in the first 11 months of 2020, implying that GDP shrunk by 2.6% y/y, according to latest figures published by the Statistical Committee of Kazakhstan.

The recorded contractions were largely in line with the expectations of international observers, such as the European Bank for Reconstruction and Development (EBRD), the World Bank and the International Monetary Fund (IMF).

According to the latest predictions by the EBRD, Kazakhstan’s economy is set to shrink by 3% in 2020 compared to the 4.5% growth recorded in 2019.

“We expect [Kazakhstan’s] domestic demand to reach its pre-crisis level only by mid-2021,” the EBRD said, adding that it expected a “5.5 per cent rebound in 2021, supported by a partial recovery of oil prices.”

The World Bank’s latest forecasting sees the Kazakh economy contracting by 2.5% in 2020 and recovering with 3.5% growth in 2021.

“Activity in Kazakhstan will likely be dampened by the waning effect of earlier fiscal stimulus, as well as weak or contracting output in key trading partners (China, Russia),” the World Bank said prior to the turn of the year.

The Russia-led Eurasian Development Bank (EDB) similarly expected Kazakh GDP to decline by 3%.

“A deeper economic contraction in the region has been avoided, largely due to government support to the population and businesses. The largest anti-crisis packages are being offered in Kazakhstan and Russia (about 8.7 and 4.5% of GDP, respectively), which have substantial fiscal reserves by regional standards,” the EDB said in a statement in December.

The EDB believes the crisis package would compensate for about 2-3% of Kazakhstan’s GDP losses in 2020. The bank also sees Kazakhstan’s growth recovering to 4.4% in 2021 as it regarded the 2020 recession as “relatively mild” for Kazakhstan.

The IMF expects a slightly weaker contraction of 2.7% for the Central Asian nation in 2020 with a 4.1% recovery in 2021.

Market research firm BCS Global Markets said in a note in December that it believes “the next 3-4 months could be quite challenging for Kazakhstan’s economy. The spread of the pandemic and a strong base factor of 4Q19 will lead to rather poor performance in many areas, especially in industry, exports, investments and domestic consumption .”

BCS sees Kazakh GDP shrinking 2.2% y/y in 2020.

“However, on our estimates, Kazakhstan could show 4.2% y/y GDP growth [in 2021],” BCS said. “The prime drivers for such a reversal will include higher output in Kazakhstan’s commodity sector (we forecast crude prices to rise by 25% from an average of $41/bbl this year to $51/bbl in 2021) and growth in domestic consumer and investment demand. A better macro environment could lead to a gradual decrease in inflationary pressures as well.”

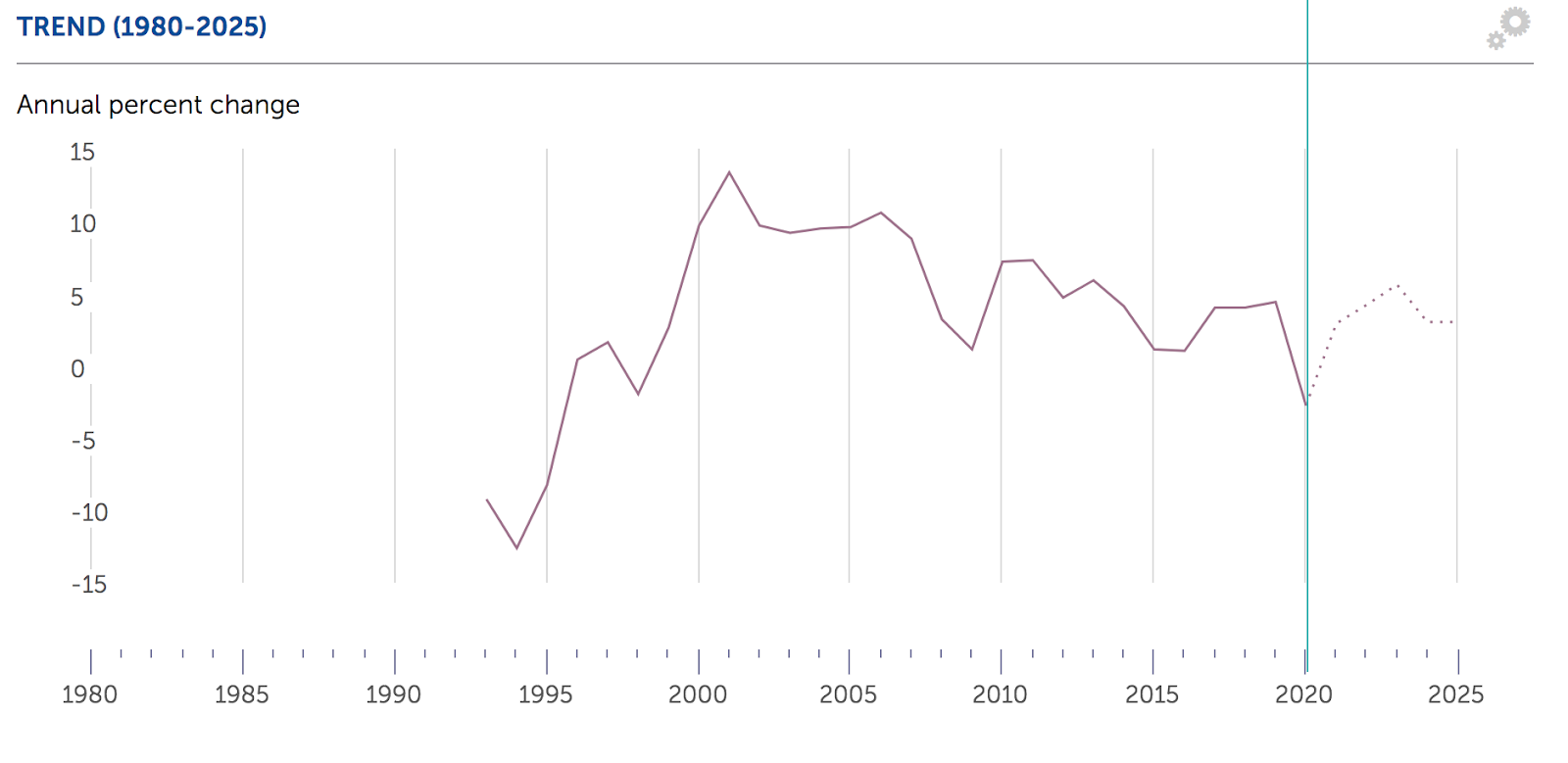

Kazakhstan, GDP growth. Source: World Economic Outlook, IMF.

- Inflation and rates

Kazakhstan's central bank in an emergency move on April 3 cut its policy rate to 9.5% from 12% to stimulate the economy amid its first national coronavirus lockdown. The regulator cut the rate further to 9% in July and has kept it unchanged since then, although it has continued to narrow its policy band.

In its latest move in December, the central bank narrowed its policy band from +/-1.5 percentage points to +/-1 percentage points. It justified the decision to keep the interest rate steady by citing the ongoing weakness in the oil market, the unresolved pandemic and uncertain expectations on the speed and efficiency of the planned mass vaccinations against the virus.

“We expect that [the National Bank of Kazakhstan (NBK)] will continue to monitor the situation and any inflation developments in 1Q21, and NBK will then start the cycle to normalize the rate afterwards. We see the base rate at 8% by YE21,” London-based broker Sova Capital said in a note.

“Passing the inflation spike could pave the way for NBK to cut rates starting from 2Q21,” Sova Capital added.

The IMF said in a statement following an official visit to the Central Asian nation in November that the National Bank of Kazakhstan’s “commitment to inflation targeting is to be commended”.

“It implies maintaining a flexible exchange rate to serve as a shock absorber as was demonstrated in the spring, while promoting policies that help reduce dollarization and implementing reforms to gradually reduce the impact of exchange rate volatility on inflation,” the IMF noted. “In this regard, enhanced policy credibility will benefit from strengthening the [central bank’s] independence, setting a credible target, and improving monetary policy transmission, which would all help better anchor inflation expectations.”

Annual consumer price index (CPI) inflation in Kazakhstan stood at 7.3% in November, according to latest data published by the country’s statistics office. The regulator was previously aiming to achieve a 4% inflation rate by 2020, but consumer prices have moved away from the upper boundary of the 4-6% inflation corridor that the central bank was maintaining. Inflation officially surpassed the 6% boundary in March, mainly driven by a sharp acceleration of prices due to increased demand caused by mobility restrictions set up in parts of the country to stop the spread of the coronavirus outbreak.

The analytical arm of Russia’s Sberbank sees Kazakhstan’s full-year inflation for 2020 coming in at around 7%, though it expects inflation to slow to 5% in 2021 given still weak consumer demand.

Real Economy

- Industry and retail

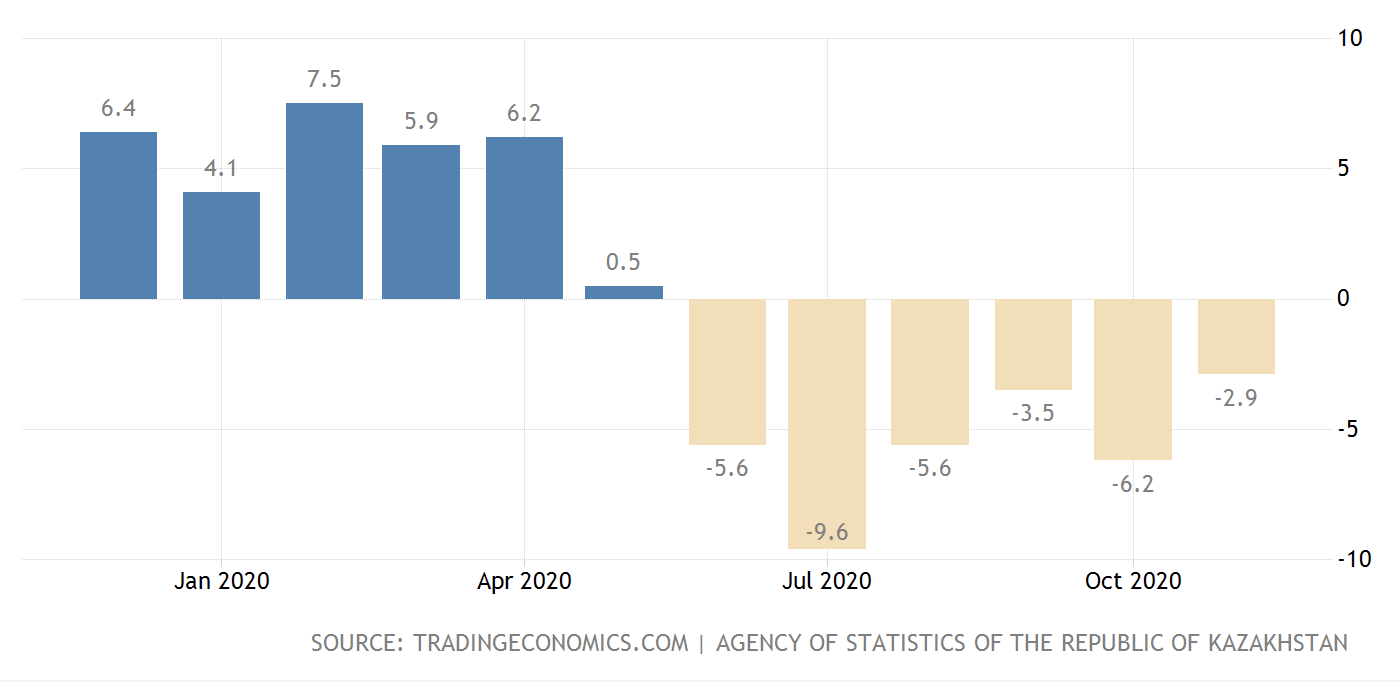

Kazakhstan's industrial output shrank 0.8% in annual terms in the first 11 months of 2020, according to latest figures released by the country's State Statistics Committee. Industrial production declined by 2.9% y/y in November alone.

The two largest sectors of the economy, oil production and ore mining, registered contractions in the period. A recovery in these two sectors in the event of the end of the pandemic in 2021 would lead to an overall upturn in industrial output. Such an outcome is probable given general expectations of a rebound in GDP growth in Kazakhstan voiced by international observers.

Kazakhstan, Industrial output by month. Source: TRADINGECONOMICS.COM, Statistical Committee of Kazakhstan.

Kazakh retail sales declined by 5% y/y in January-November, reaching a value of Kazakhstani tenge (KZT) 10,101.8bn (€19.87bn), according to latest data published by Kazakhstan's State Statistics Committee. The plunge reflected a decline in consumption driven by stalled business activity amid pandemic lockdowns.

In November alone, retail sales grew by 0.7%, the figures showed. This reflected an ongoing recovery as strict coronavirus lockdown measures were lifted in September.

Kazakhstan, Retail trade growth by month. Source: Statistical Committee of Kazakhstan.

- Oil and Gas

Oil output fell by 4.8% y/y to 78.5mn tonnes in January-November. Oil production this year was originally expected to stay unchanged from last year, but this planned trajectory is set to change due to Kazakhstan’s commitments to cut production, made as part of an OPEC+ agreement struck as world oil prices began to collapse. Kazakhstan complied with its commitments to cuts at a rate of 98% in November.

Kazakh state-run oil and gas producer KazMunayGas (KMG) saw its net income decline 42.24% y/y to Kazakhstani tenge (KZT) 116bn (€227.8mn) in the third quarter of 2020, according to KMG’s quarterly results. KMG reported a 7% decline in its output and shares in output at three giant Kazakh oilfields (Tengiz, Kashagan and Karachaganak) to 449,000 barrels per day (bpd) between January and September. The Chevron-led Tengizchevroil joint venture led by KMG has been affected the most by the fall in oil output, with a decline of 8% to 117,000 bpd.

KMG has set the goal of producing 21.7mn tonnes of oil in 2021, unchanged from 2020, provided OPEC+ restrictions remain, the deputy chairman of the board for economy and finance at KMG, Dauren Karabayev, has said. The company’s budget for 2021 is based on the price of $40 per barrel of Brent. Similarly, the energy ministry has set total oil production in the country at 85mn-86mn tonnes for 2021, unchanged from 2020 and down from 90mn tonnes in 2019.

The OPEC+ group’s agreement to raise their collective oil output by 500,000 barrels per day (bpd) in January may signal that Kazakhstan and KMG might change their output targets for 2021. If the end of the pandemic and associated projections of economic recovery come true, the possibility of a revision is highly likely.

In a positive development for Kazakhstan, the Karachaganak Petroleum Operating (KPO) consortium managing one of Kazakhstan’s biggest oil and gas fields has paid $1.3bn to settle a long-running dispute with the Kazakh government over profit-sharing. The agreement paves the way for the project’s investors to push ahead with a $1bn expansion project.

The energy ministry announced on December 14 that in addition to the $1.3bn cash settlement, KPO agreed to adjust the production-sharing agreement (PSA) for the Karachaganak field. This will earn the Kazakh state an extra $600mn in oil and gas sales by 2037, assuming a $40-50 per barrel crude price.

- Mining

Ore mining fell by 5.5% y/y to 106mn tonnes in January-November 2020 amid lower demand for commodities such as copper in the year largely as a result of the pandemic.

A major player in the Kazakh mining industry is copper producer KAZ Minerals, which was subject to a wave of downgrades by stock analysts throughout August-October.

They included Liberum Capital’s assignment of a "hold" rating from a "buy" rating in late October. Zacks Investment Research lowered KAZ Minerals from a "buy" rating to a "hold" in a research note on October 27, while JPMorgan reaffirmed a "neutral" rating on shares of KAZ Minerals on October 7. Earlier reports included Credit Suisse Group’s upgrade for KAZ Minerals to a "neutral" rating from an "underperform" rating in August followed by Morgan Stanley’s reaffirmation of an "overweight" rating on September 24.

Following the downgrades, KAZ Minerals announced a £3bn all-cash buyout offer for its shareholders with the intention of taking the company private, though the plan is related to its Baimskaya project in Russia and thus does not reflect the state of the Kazakh copper mining sector. The takeover of KAZ would be completed by mid-2021 under outlined plans.

Another segment of the Kazakh mining sector, namely uranium mining in which the ex-Soviet state is the biggest producer, experienced production cutbacks made in March 2020 by state-controlled Kazatomprom, leading to a growing supply-demand imbalance and a rise in global uranium prices. The COVID-19-based cutbacks saw the uranium price jump by over 40% between March and May, when Canadian uranium producer Cameco initiated its first temporary shutdown of Cigar Lake. A second shut-down at Cigar Lake is expected to push up the price once again in a trend that may potentially last through early 2021.

- Agriculture

The government was able to ensure stable foodstuff supplies to domestic and foreign markets in 2020 despite the pandemic, according to Minister of Agriculture Saparkhan Omarov.

Kazakhstan exported food products worth $1.3bn to Shanghai Cooperation Organisation (SCO) countries in the first eight months of 2020. The SCO countries include neighbouring Central Asian countries along with Russia and China. These account for the majority of Kazakhstan’s food exports.

Agricultural production in Kazakhstan grew by 5% in the first nine months of the year in spite of global constraints brought about by the pandemic.

The developments were in line with Kazakhstan’s objective to diversify its economy away from over-reliance on oil exports with a heavy focus on the agriculture sector and food exports to neighbouring China.

The government has been sticking to its pledge to pump KZT423bn (€1.2bn) into the country's grain industry during 2017-2021 as part of a programme to improve industry profitability by 30%-40%. That includes ongoing efforts to shift exports toward oilseeds and pulses and away from wheat.

Omarov said in August that Kazakhstan’s export potential for grain and flour stands at 7.5-8mn for the 2020-2021 marketing year. Kazakh Grain Union board member Alexander Malov said in September that Kazakhstan may export 6.7mn tonnes of wheat and wheat flour in the 2020-2021 marketing season, up from 6.6mn tonnes in the previous season.

Yet the coronavirus has not left the CIS country’s agriculture sector unscathed. Kazakhstan produced 2.6bn eggs in the first six months of 2020, down by 5.6% y/y, and the country is potentially expected to produce 3bn eggs by end-2020, down from 4.5bn in 2019, the Kazakh Egg Producers Association has warned. The news came as the pandemic was driving some farms out of operation and others into culling their stock, as the entire Kazakh poultry industry is feeling the heat from high prices on the domestic grain market. The price hike came about after quotas on grain exports were introduced by the government to ensure food security amid lockdowns.

The poultry segment was also late in 2020 hit hard by the death of over 1.2mn birds at three industrial poultry farms due to an avian flu outbreak. When combined with the pandemic-derived issues, this looked likely to harm poultry and egg production further in 2021.

- Manufacturing

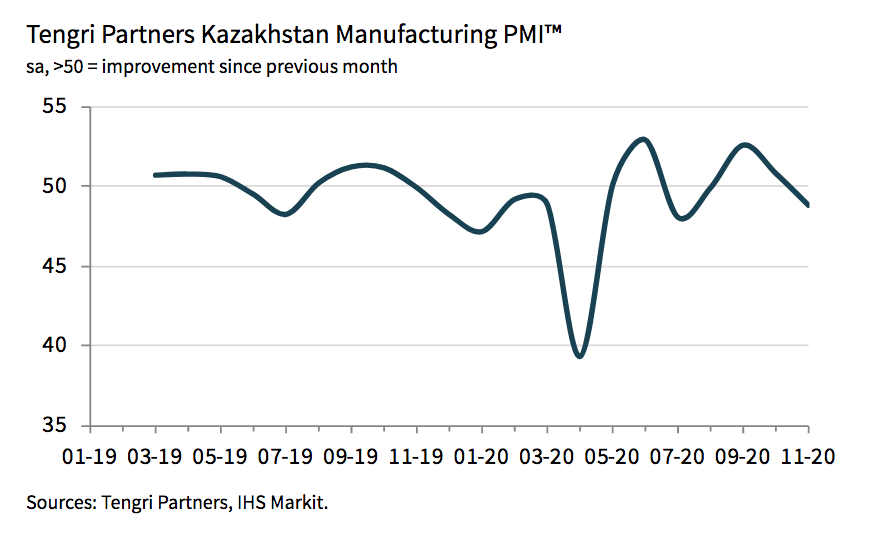

Operating conditions across the Kazakh manufacturing sector experienced a renewed deterioration in November, hitting a four-month low, according to the latest Tengri Partners Kazakhstan Manufacturing Purchasing Managers’ Index (PMI). The index posted 48.8 in November, down from 52.6 in October, the PMI survey report released by IHS Markit showed on December 2.

Anything above 50.0 signifies an overall expansion and anything below 50.0 represents a deterioration. The survey panellists linked much of the downward trend in November to renewed contractions in both output and order book volumes.

As such, expectations of growth in the sector within the next 12 months have been declining. Operating conditions in the sector will nevertheless improve in the event of the global pandemic ending as expected in 2021.

Financial policy outlook (budget & borrowing)

The International Monetary Fund (IMF) expects Kazakhstan to register a fiscal deficit of 3% of GDP in 2021, down from 2020’s projected 5.4%.

“Lower oil prices and lower global energy demand affected Kazakhstan’s external balances in 2Q20 and 3Q20. Lower energy proceeds and lockdowns forced authorities to spend more from the [national rainy day fund] NFRK, widening the support to the budget from 5% of GDP to 8% of GDP in 2020,” SOVA Capital said in note.

It added: "This level of support will remain elevated into 2021, on our estimates.”

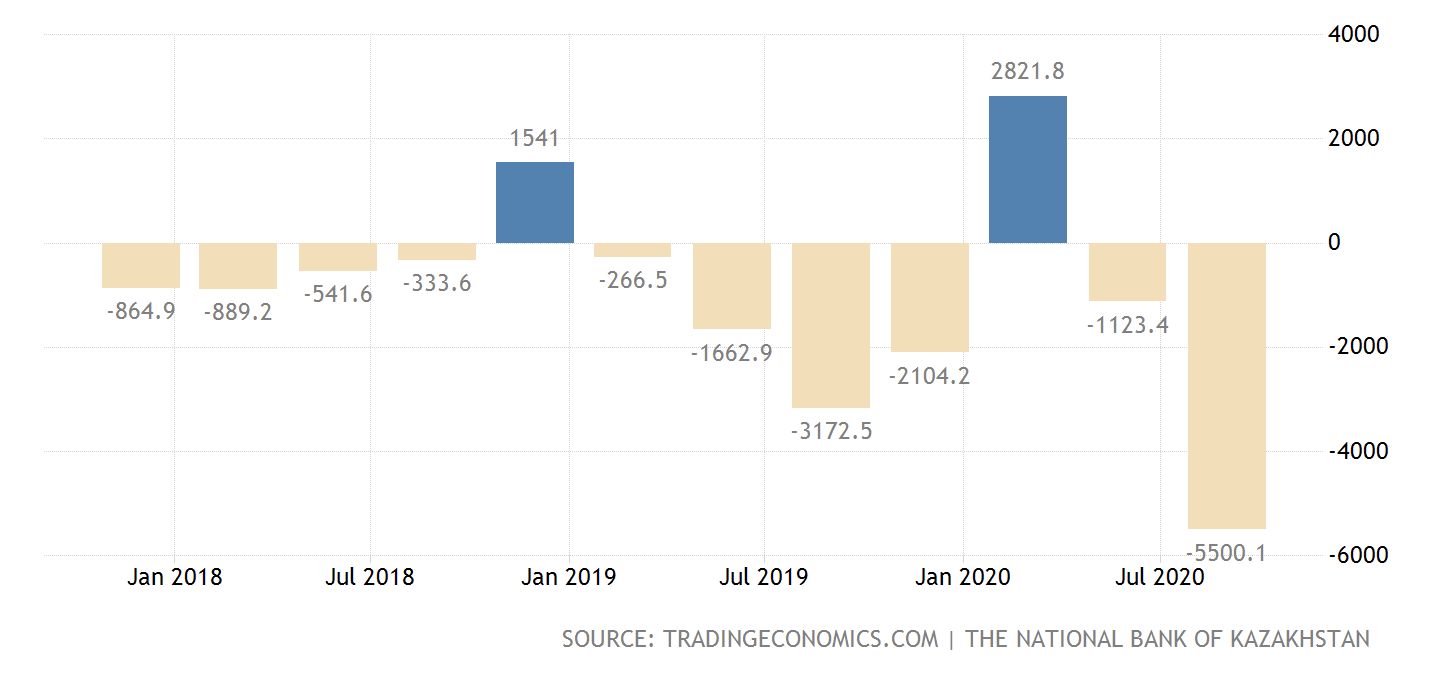

The central bank released in December its preliminary balance of payments estimates for the third quarter of 2020, with the deficit widening to $5.5bn from $1.1bn in the second quarter. This was partly driven by a 30% drop in global oil prices on an annual basis seen in the third quarter of 2020, which led to a 36% y/y decline in Kazakhstan’s exports in the third quarter.

Kazakhstan announced in late November 2020 that it intends to borrow €908.6mn from the Asian Development Bank (ADB) and €661.8mn from the Asian Infrastructure Investment Bank (AIIB) to finance its 2021 budget deficit and address pandemic impacts on the economy. Finance Minister Yerulan Zhamaubayev told parliament both loans were part of the two banks' COVID-19 packages.

Such borrowing may expand further in 2021, as authorities worry that projected budget deficits over the next several years may bring the nation's rainy-day National Fund close to its minimum balance, removing the government’s ability to tap into it.

The government plans to rely heavily on the $65bn fund in upcoming years to fill budget gaps. Kazakhstan intended to draw approximately $11.5bn out of the fund in 2020 and $8.9bn next year. The central bank governor Yerbolat Dosayev told a government meeting in August that despite growing nominally the fund was expected to shrink in proportion to GDP.

“As a result, by the end of 2023 National Fund assets will stand at 30.8% of GDP, approaching the minimum balance of 30% of GDP,” Dosayev said. As such, the governor urged the cabinet to implement measures under the new counter-cyclical budget rules to reduce the deficit.

Kazakhstan, Balance of payments (in millions of USD). Source: TRADINGECONOMICS.COM, The National Bank of Kazakhstan.

Markets outlook

- Stock market

Kazakhstan’s Astana International Exchange (AIX), launched as part of Astana Intenrational Financial Centre (AIFC) in 2015, continued with efforts to draw much needed liquidity in 2020. Some of the milestones of the year for AIX included debut green bonds, the listing of the AIX's first Chinese yuan-denominated (RMB-denominated) bond and the listing of London-listed Ferro-Alloy Resources.

The bourse also listed shares of Bank Center Credit (BCC), which became the first issuer listed on AIX based on Regional Equity Market Segment (REMS) - introduced in 2020 - which aims to grant mid-cap companies access to a broader investor base and to the equity capital market.

In November, AIX in partnership with Kazakh investment firm BCC Invest announced the listing of new exchange-traded notes. They are BCC Global Exchange Traded Notes (ETNs) linked to the performance of one of Kazakhstan’s largest interval mutual funds, “CenterCredit-Valyutniy”.

The notes are issued by a special purpose company, Global Fund A SPC Limited, with sole assets as units in the interval mutual fund and cash. The notes will be traded on the AIX with BCC Invest acting as a market maker, granting liquidity and easy access for investors. Subsidiary Bank Sberbank of Russia in Kazakhstan will take on the role of a custodian bank that will provide safekeeping for underlying assets. CROWE Kazakhstan has been appointed as the special purpose company’s auditor firm.

In December, Kazakhstan’s Agency for Regulation and Development of the Financial Market approved amendments to ensure that Kazakh institutional investors are now able to trade on the AIX and hold AIX-listed securities denominated in the Kazakhstani tenge (KZT) under the same prudential requirements as with other currenies, AIX announced in a statement. Thanks to the amendments, financial institutions, including banks, insurance companies, investment funds and brokerage firms, are now able to acquire publicly traded AIX shares and other securities of Kazakh firms denominated in tenge. Previously, institutions were only allowed to purchase AIX foreign currency-denominated securities.

“Development and integration of the securities market are essential conditions for sustainable economic growth of the country. We are pleased that Kazakhstani institutional investors will be given the opportunity to replenish their asset portfolio with shares of Kazakhstani companies listed on AIX. Investments in the 'national champions' of Kazakhstan will undoubtedly contribute to business growth, and will also favorably affect the development of the equity market and the national economy as a whole,” Tim Bennett, CEO of AIX, commented.

Among all AIX-related developments in 2020, the bourse undoubtedly benefited substantially from the double-listing of Kazakh fintech firm Kaspi.kz’s initial public offering (IPO) on the London Stock Exchange (LSE) and the AIX. The IPO valued Kaspi (KSPI) at $6.5bn, the highest price tag ever given to a publicly listed Kazakh company. The IPO was the LSE’s second largest of the year and the fourth largest in all of Europe.

AIX is expected to continue hunting for liquidity in 2021, including adopting regulatory changes that would turn the bourse into a functional securities exchange market as compared to the Kazakhstan Securities Exchange (KASE) in Almaty, which was Kazakhstan’s first failed attempt at kicking off a bourse. Much of AIX’s endeavours will rely on the Kazakh government’s willingness to continue IPOs of stakes in major state-owned firms. The big privatisation programme has continued to suffer post-ponements introduced by authorities due to a lack of favourable market conditions in the past few years. Given the situation with the pandemic and associated uncertainties, it is likely that authorities may postpone the planned listings once again in 2021.

- Currency

The IMF urged Kazakhstan in November to enhance the credibility of the central bank’s monetary policy following a tightening of foreign exchange regulations amid weak world oil prices.

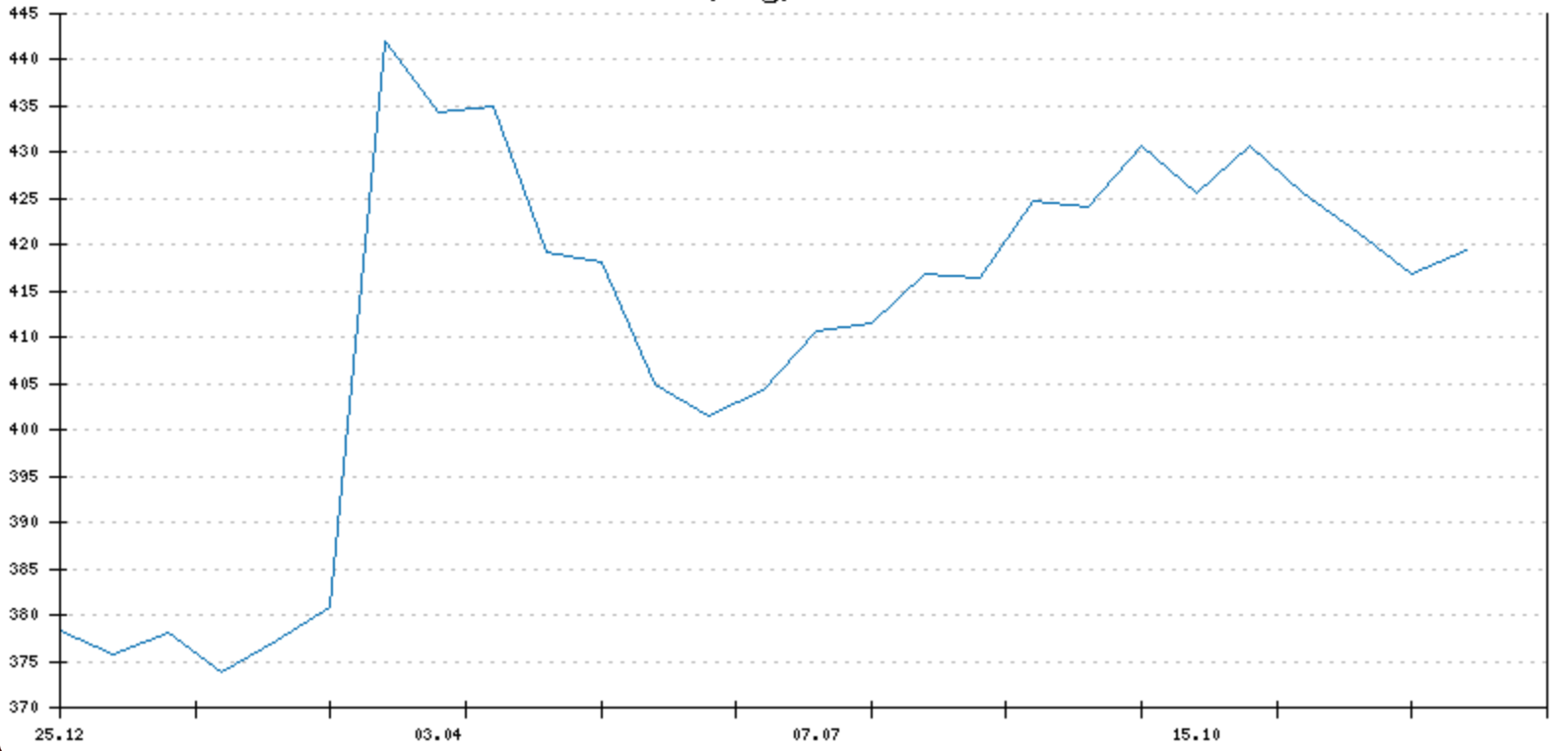

The Kazakh tenge’s strength relies heavily on hydrocarbon prices with oil Kazakhstan’s primary export. Despite a nominally freely floating exchange rate, the regulator took on measures this year to prop up the national currency, including direct interventions by the central bank and foreign currency sales by the Kazakh sovereign wealth fund and state-run firms. It also set tighter restrictions on forex purchases by local businesses. The tenge lost over 10% of its value against the greenback in March, reaching historic lows below KZT440, but it has slightly recovered since then. The stability of the tenge is a top political issue in Kazakhstan.

BCS said in a note that stronger oil prices, which the analytical firm predicts for 2021 amid the expected end of the pandemic, “should lead to a moderate appreciation of [the tenge] next year.”

The tenge was stabilising at around KZT420 against the greenback towards the end of 2020, registering KZT419.89 to the dollar as of the end of December 24.

“The dissipation of geopolitical risks could push the KZT/$ rate to 410by YE21,” Sova Capital said in a note on December 9.

Kazakhstan, KZT rate against USD. Source: The National Bank of Kazakhstan. Chart source: Yahoo! Finance.

- Banks

In late November, Fitch Ratings revised its outlooks on Kazakhstan’s Halyk Bank (Halyk), Halyk Finance (HF), Alfa Bank (ABK) and ForteBank (Forte) to stable from negative. The long-term issuer default ratings (IDRs) were affirmed at 'BB+' for Halyk and HF, 'BB-' for ABK, and 'B' for Forte. Fitch also affirmed Subsidiary Bank Sberbank of Russia (SBK) at 'BBB-' with a stable outlook.

The revision of the outlooks and affirmation of ratings on Halyk, ABK and Forte were due to Fitch's view that “the banks' strong pre-impairment profitability and substantial capital buffers will be sufficient to mitigate the ongoing pressure on their asset quality, stemming from the economic recession, lower oil prices, and negative implications from the spread of COVID-19 on the broader economy”. Fitch maintained its negative outlook on the overall operating environment in Kazakhstan, but believed that the ratings of Halyk, ABK and Forte could tolerate a more than previously anticipated severity in increasing loan impairment charges (LICs).

Not all observers share Fitch’s optimism.

“The [Kazakh] banking system, despite having weathered the pandemic’s adverse effects so far, remains fragile with relatively high levels of dollarization,” analytical firm RAEX-Europe said in a note in December.

Ratings agency Moody's changed its outlook on Kazakhstan's banking system in April to negative from positive due to what it saw as growing asset quality risks in the sector and pressure on profitability. Moody’s saw the coronavirus outbreak-driven tighter monetary conditions and slower economic growth along with weak global oil prices leading to a reduction in loan demand and weakening of borrowers' ability to service debt, as problem loan ratios are expected to grow across the sector, agency said.

Higher credit costs, pressure on net interest margins and losses on fixed income securities were expected to weaken profitability in the Kazakh banking system, though liquidity is expected continue standing strong, Moody’s noted. The ratings agency also pointed out that depositors at the largest Kazakh banks will continue to benefit from government support due to the system's small size and the government's ample fiscal capacity.

Meanwhile, Kazakhstan’s banking sector continued to consolidate in 2020. Kazakhstan-based Jysan Bank (formerly Tsesnabank) recently agreed to acquire competitor ATF Bank from Galymzhan Yessenov, its sole shareholder, turning Jysan into Kazakhstan’s second-largest bank by assets. The largest Kazakh lender Halyk Bank currently controls 32% of the country’s banking sector, while Jysan will gain a 10% share. This also means that the seven largest Kazakh banks will control 78% of the Central Asian nation’s banking market.

It is not unreasonable to expect this consolidation process to continue in 2021.

- Foreign investment

The gross inflow of foreign direct investment (FDI) into Kazakhstan’s economy amounted to $3.6bn in the first quarter of 2020, local analytical agency Finprom said in September. The first quarter accounts only for FDI received prior to the introduction of major lockdown measures against the pandemic and the resulting economic decline in the country. The top three investors in Kazakhstan in the period were given as the Netherlands ($988.3mn), the US ($744.9mn) and Russia ($379.9mn).

FDI inflows likely weakened during the pandemic, but as the pandemic is expected to end in 2021, Kazakhstan will likewise see a recovery in FDI.

One FDI highlight for Kazakhstan in 2021 is the Cyprus-Kazakhstan Double Taxation Treaty coming into effect on 17 January 2021. The development is expected to create a channel for investment from Kazakhstan through Cyprus to Europe. Cyprus stands as one of the top 10 investors in Kazakhstan.