_0_1781255241.jpg)

_1781191847.jpg)

Fujimori wins Peru on votes from Peruvians who don't live there

1 hour ago

It would seem that Kazakhs cannot get enough of buy-now-pay-laters (BNPLs)—and that is a big headache for officials charged with keeping a lid on inflation and restraining consumer debt growth.

The rise of the BNPL, a facility that provides a short-term loan with no, or a low, interest rate, has come hand in hand with Kazakhstan and the Central Asia region’s emergence as an e-commerce hub. Consumers have reaped benefits, but the economic czars of Kazakhstan, Central Asia’s largest economy, are increasingly paying attention to seldom-discussed downsides.

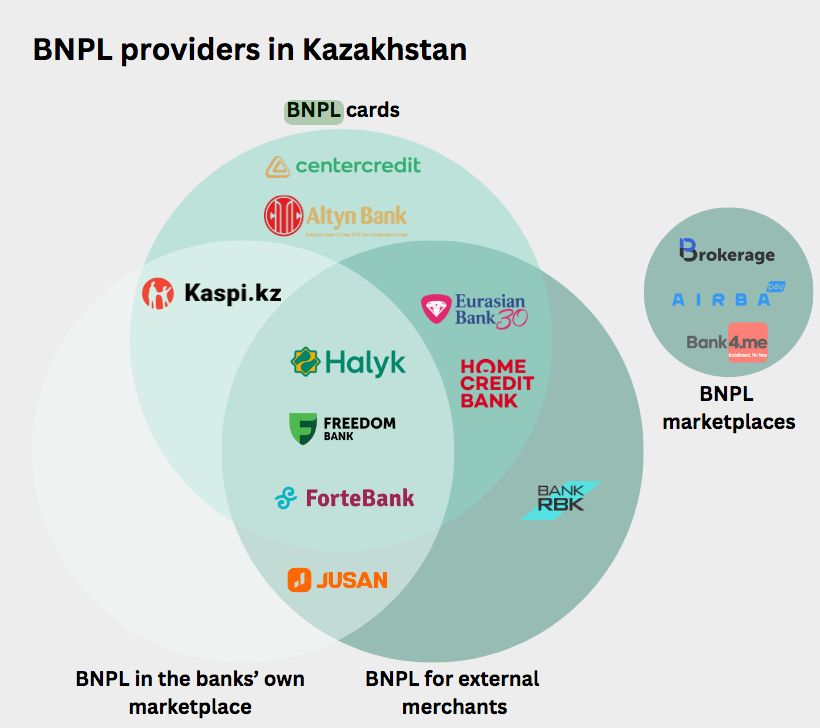

Anyone who diligently follows fintech knows about the breakout success of Kaspi.kz and its listings in London and on the Nasdaq. But the new forms of credit popularised by digital service providers like Kaspi.kz could in the long run ail the country’s banking sector and economy.

In December, a report from Bloomberg revealed how the popularity of BNPL financing in Kazakhstan’s online marketplaces had attracted regulatory scrutiny, with anxieties over impacts on inflation and the consumer debt metrics. BNPL, a short-term payment deferral option, had become a significant revenue source for lenders like Kaspi.kz and Halyk Savings Bank, which earn commissions from such transactions, the report noted. Indeed, Kazakhstan's digital marketplace sales grew 60% last year, reaching KZT1.77tn ($3.7bn). Kaspi.kz, whose online marketplace dominates over 75% of the sector, has even described BNPL as its most critical product, accounting for nearly half of its lending last year.

Kazakh lenders’ BNPL portfolios hit KZT2.3tn ($4.5bn) as of September 2024, representing a 17% year-to-date increase, according to figures provided by the Agency of the Republic of Kazakhstan for Regulation and Development of the Financial Market (ARDFM) cited by Bloomberg.

Source: RISE Research’s analysis, ARDFM, ADL Report

The booming state of the BNPL market extends beyond Kazakhstan. Fintech Global reported on February 3 that, according to a recent report from ResearchAndMarkets.com, the BNPL market globally was valued at $141.8bn in 2021 and is projected to grow at a 33% compound annual growth rate (CAGR) until 2026. It also cited a report from Juniper Research, which assessed that the number of BNPL users will grow to above 900mn worldwide by 2027, up from 360mn recorded in 2022.

In Kazakhstan, ARDFM is among those that have raised concerns that BNPL and related pricing practices may inflate prices across the board and undermine efforts to curb household debt.

The World Bank and local Kazakh experts, meanwhile, have also issued warnings that the ease of accessing instalment credit may result in high household debt levels and increased financial strain.

BNPL-driven overindebtedness and inflation

The National Payments Corporation of Kazakhstan (NPCK) said in its Fintech Report 2024 that BNPLs may account for 50% of consumer loans in the country, according to anecdotal evidence, though official statistics make it hard to confirm this figure. It is worth observing that consumer lending grew by 34-42% annually in 2022-2023, which could have been significantly driven by BNPLs.

By 2023, some banks were aggressively extending consumer loans (including BNPLs) to even riskier borrowers, sharply boosting debt loads – a trend that will “sooner or later” spur a rise in loan defaults, economist Alexander Yurin told LSM.kz.

“In June of last year, the maximum interest rates on secured loans and mortgage loans were reduced to 40% and 25%, respectively. However, the maximum rate on microloans and unsecured loans remained at 56%. The problem is that a high maximum rate allows banks to inflate actual loan interest rates. This, in turn, enables them to shift credit risk onto borrowers across the entire pool of consumer loans.

“Conscientious borrowers effectively compensate out of their own pockets for bank losses resulting from defaults, while financial institutions can issue riskier products. In this situation, lowering the maximum rate to 40% would likely still be insufficient," Yurin noted.

Yurin advocated for stricter regulations in the consumer lending sector to address growth in non-performing loans (NPLs). He specifically suggested tightening oversight on interest-free loans and BNPL instalment plans. Drawing from Russia’s approach to limiting financial services for consumers, he proposed a requirement for buyers to be informed of the actual cost of an instalment plan at the time of purchase, as this information is often hidden from them.

"De facto, instalment purchase schemes can increase the final cost of a product for the buyer by 1.5 times or more, forcing even those who do not use instalment plans and pay in a lump sum to purchase goods at inflated prices," he noted.

The ARDFM is concerned by agreements between BNPL providers and vendors to keep cash prices at the same level as BNPL prices. Such deals mean consumers are persuaded that they may as well pay in instalments. They perceive that paying a lump cash sum for the product cannot offer any financial gain. But if a BNPL price has been inflated by hidden fees that a cash price must reflect, it means the buyer is denied a lower price that should be available to someone who pays in cash.

Madina Abylkasymova, head of the ARDFM, is among those that have argued it is the inflationary hidden fees in BNPL agreements that often result in cash buyers paying the same as those opting for financing,

In 2023, Kazakh banking sector expert Galim Khusainov critiqued in an op-ed written for Ratel.kz the absence of BNPL oversight – arguing that without action, these instalment schemes will continue to fuel inflation and over-indebtedness while reducing market competition. Similarly to Yurin, Khusainov believes that consumers need to be informed about the hidden BNPL interest rates.

“Today, even people who don’t need loans are opting for instalment plans, thinking it’s a beneficial solution. While there is some truth to this due to the lack of market information about the product, in reality, if consumers were given the choice to either buy with a discount or through an instalment plan with an embedded interest rate, those who are financially capable would choose the discount,” Khusainov wrote.

“The biggest problem in Kazakhstan is that you can now buy even toilet paper via instalment plans, and in the cost of the product, the bank’s interest margin is built in. There is absolutely no regulation for BNPL,” Khusainov wrote.

Despite these concerns, BNPL continues to be favoured by both consumers and merchants, with some vendors reporting up to a 30% decline in sales without the financing option. Local banks and fintech companies typically defend the single-price approach, arguing that it enhances the customer experience.

BNPL-inflation death spiral

According to a Bank of International Settlements (BIS) study, “compared with traditional consumer credit, BNPL users are typically younger, with less education, more debt, lower credit scores and higher delinquency rates.”

BIS also noted that BNPL is more widespread in countries with greater e-commerce penetration and higher inflation. Kazakhstan fits the bill here as the Central Asian country experienced double digit inflation, impacted by the COVID-19 crisis and the war in Ukraine, until the end of 2023. And even when inflation fell slightly below double digits, double-digit inflation perceptions persisted among Kazakh citizens. Kazakhstan’s central bank reported that perceived inflation among the population rose to 14.6% in December.

Since BNPLs feed inflation, and inflation feeds BNPL demand, there is potential here for a sort of a BNPL-inflation death spiral that will inevitably harm BNPL providers themselves.

Richard Wray, COO at payment processor Carta Worldwide, told Fintech Global last year: “High interest rates are a double-edged sword. On the one hand it will encourage more consumers to embrace BNPL over other forms of credit like credit cards because the interest free rate periods of BNPL become more attractive in a high-rate environment. On the other hand, it puts a squeeze on BNPL providers raising money to lend from the debt market. When we combine higher costs of funding credit with the drop in consumer spending that we’re seeing as a result of inflation and falling real term wages, providers will see a significant impact on revenues.”

Given these trends, supporting the regulation of BNPLs might be in the interests of both the Kazakh consumer and the BNPL provider.

Kazakhstan's financial market regulator is currently working with the nation's competition regulator to ensure lower prices for cash payments and compliance with caps on retail lending rates. However, while the financial regulator is pushing for changes to marketplace practices, the competition authority has yet to take a firm stance.

The IntelliNews PRO service includes access to reports, exclusive market data, and more news that decision-makers care about. Stay ahead of the market with IntelliNews PRO.

Sign Up Now