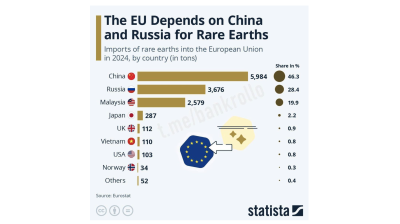

EU rare earth supply dominated by China and Russia - Eurostat

4 hours ago

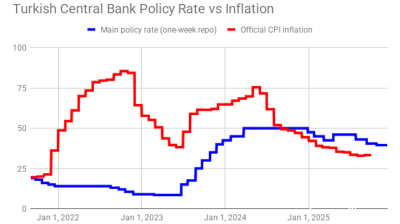

Turkey’s annual consumer price index (CPI) inflation edged down to 18.71% in May from 19.50% y/y in April, the Turkish Statistical Institute (TUIK) said on June 3. The official inflation rate in May was thus recorded at its lowest point since last August’s 17.9%.

The official data suggests that the latest bout of lira depreciation did not negatively impact inflation.

In the run-up to the inflation data release, a Bloomberg poll predicted headline inflation for the fifth month of the year would come in at 19.3% y/y.

The official inflation data for May also showed that food inflation, which takes the biggest weighting in Turkey’s CPI basket at 23.29%, saw a substantial decline of 1.18% m/m, bringing the annual food inflation increase to 28.44% from 31.86% y/y in April.

It is curious that when fresh vegetable prices boom during the winter months they do not have a significant affect in the headline CPI, but when they fall during the spring the impact is felt in the indicator.

Listed inflation for alcoholic beverages and tobacco—which only account for a 4.23% basket weighting—jumped again, from 9.66% y/y in April to 19.22% y/y in May. Big tax hikes caused that impact in the official figures, just as the pressure from food inflation eased.

Official healthcare prices rose at an annual rate of 19.37% in May compared to 19.75% in April. The health ministry last month hiked the fixed exchange rate for imported pharmaceutical products by 26.4%. Healthcare prices have the second lowest basket weighting, of 2.58%.

Official transportation prices, which have the second largest basket weighting of 16.78%, rose by 12.40% y/y, lower than the 12.55% y/y seen in April, while official housing and utilities prices, which have the third largest basket weighting, of 15.16%, rose 14.68% y/y, down from the 15.31% y/y recorded in the fourth month.

The average prices of 48 items in TUIK’s inflation basket of 418 items remained unchanged in May while those of 267 items increased and those of 103 items decreased. It is notable that the official data points to widespread rises in CPI basket item prices but the impacts do not show through in the headline inflation figure.

Official domestic producer price inflation (PPI) in May edged down to 28.72% y/y, the lowest level seen since July’s 25% y/y, TUIK said in a separate press release.

Official PPI for energy rose by 39% y/y, down from April’s 47.55% y/y.

“The weaker-than-expected Turkish inflation figures for May, combined with the recent rally in the lira, means that the monetary policy committee will continue to shift away from its hawkish stance at this month’s policy meeting [to be held on June 12]. But with a number of flashpoints on the horizon for the currency in the coming weeks, including the upcoming Istanbul mayoral election [revote after the annulling of the opposition’s end-of-March victory], there is little scope for policy easing,” Jason Tuvey of Capital Economics said in a research note.

Last month, Turkey’s banking regulator, the BDDK, requested that banks wait one day before settling retail FX transactions valued at over $100,000. The previous practice was to settle on the same day. The decision was seen as the latest in a series of measures aimed at easing pressure on the lira ahead of the Istanbul mayoral election re-run.

“Steps taken [last month] by Turkish officials to shore up the lira could be the first move towards the imposition of capital controls, but we doubt these would be effective. If anything, they would probably store up larger falls in the currency,” Tuvey said on May 24 in a separate research note entitled “Turkey edging towards capital controls”.

Tuvey added: “The evidence from other countries is that capital controls tend to work best when the state has strong control over the financial system in order to prevent leakages and when controls are focussed on restricting residents’ ability to take money out of the country. In Turkey’s case, it’s not clear that officials have the necessary experience or infrastructure in place to prevent leakages.

“Meanwhile, resident capital outflows are small and fears that controls could be widened would probably deter foreign investors. More fundamentally, capital controls wouldn’t tackle the problem caused by high inflation, which means that the nominal lira exchange rate needs to fall. A rise in the real effective exchange rate and an erosion of competitiveness would depress exports and encourage imports, causing the current account position to worsen.

“Low FX reserves mean that officials wouldn’t be able to mount a credible defence of the lira; higher interest rates would be needed to attract capital inflows to fund a wider external shortfall. This would result in weak economic growth and the lira would eventually face a sharp adjustment anyway.”