Ever in India’s shadow, Bangladesh needs to define its own energy path

16 minutes ago

Politics

An alliance of the Social Democrats (PSD) with the Liberals (PNL) is expected to rule Romania for the coming three years, until the super-electoral year 2024.

The unexpected coalition between Romania’s main centre-left and centre-right parties was formed after several months of deep political crisis after the breakup of the former centre-right coalition formed by the PNL and Union Save Romania (USR). The earlier coalition was seen at the time of its formation as the end of the Social Democrats’ influence, at least temporarily, even though the PSD is the largest party in the current parliament. Yet just a couple of years later, the PSD was back in power alongside the PNL after the latter fell out with its reformist junior coalition partner.

The political crisis in September-November 2021 and the alliance that followed it put an end to the electorate’s hopes for quick democratic and economic advancements particularly in the area of rule of law, driven by USR. Nonetheless, Bucharest will be under pressure to keep up the pace of reforms and economic stabilisation from both the National Recovery and Resilience Plan (PNRR), already approved by the European Commission after being sketched during the short-lived reformist centre-right government, and the Excessive Deficit Procedure (EDP) that was suspended during the pandemic but still includes tight targets including a general government deficit of under 3% of GDP by 2024.

This framework provides some stability as regards the future policies pursued (budget planning, public administration modernisation), given the targets and the milestones included in the PNRR.

On the downside, the commitment to reforms and the credibility.of the new alliance are at least debatable. The National Liberal Party has no leader after prime minister Florin Citu won the party's internal elections but lost the prime minister seat. The Social Democrats are no longer headed by politicians under investigation for corruption, but it hasn’t undergone deep internal reforms towards becoming a genuine social democratic party many Romanians, facing the widest income discrepancies in Europe, might welcome.

The collapse of the centre right alliance formed by Liberals with reformist USR is highly relevant in the process of defining expectations. Officially, USR blamed Citu for allocating some €10bn “helicopter money” to local administration, in exchange for political support. Unofficially, USR and President Klaus Iohannis argued over who should appoint the head prosecutors. Iohannis went on to deepen the crisis though his unwavering support for Citu.

In the absence of a robust domestic reformist administration, the milestones, targets and the budget consolidation trajectory negotiated with the European Commission remain Romania’s main anchors over the coming years. Other targets, such as the adoption of the euro and Schengen area membership, remain in limbo.

The government itself, controlled by the Social Democrats but incorporating Liberal elements as well, has sketched a model of economic growth based on local capital (supported by the PSD) and more manufacturing and investments (required by the PNL) that focuses to a lesser extent on foreign direct investment. Encouraging local capital is economically sustainable and profitable in terms of Gross National Income. But the real challenge concerns the design and implementation of such a strategy that exists so far only at the level of petty political rhetoric.

Macroeconomy

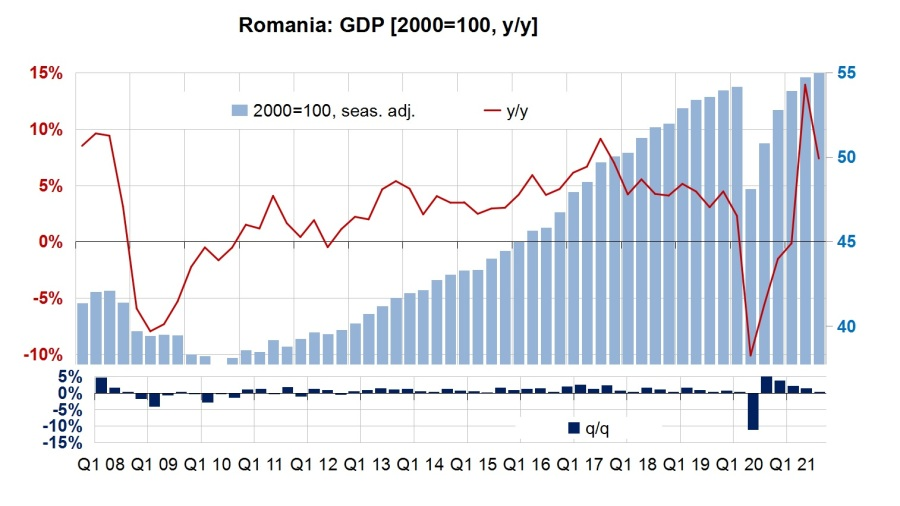

GDP growth: Analysts have revised downwards their estimates for Romania’s economic growth in 2021 to below 7%, in response to the Q3 flash GDP estimate issued on November 16.

The government expects 7% economic growth in 2021, followed by a 4.6% advance in 2022. The growth would remain around 5%, according to the official forecast.

The European Commission sees 5.1-5.2% economic growth in Romania over the coming two years, according to its November 11 Autumn Forecast.

Romania’s economic growth eased to 7.4% y/y in the third quarter of 2021 from 13.9% y/y in Q2, while the average annual growth rate for the January-September period was 7.1% y/y.

In its Autumn Forecast, the Commission slightly altered its forecast for Romania’s growth outlook, largely shaped by the Recovery and Resilience Programme. The 2021 growth forecast was revised slightly downwards to 7% (from 7.4% in the Summer Forecast) while 2022’s projection was revised upwards to 5.1% from 4.9%.

“Whereas the effect of pent-up demand on private consumption is expected to fade out [in 2022-2023], growth is set to remain positive thanks to growing employment, falling inflation and robust wage growth,” the Commission said.

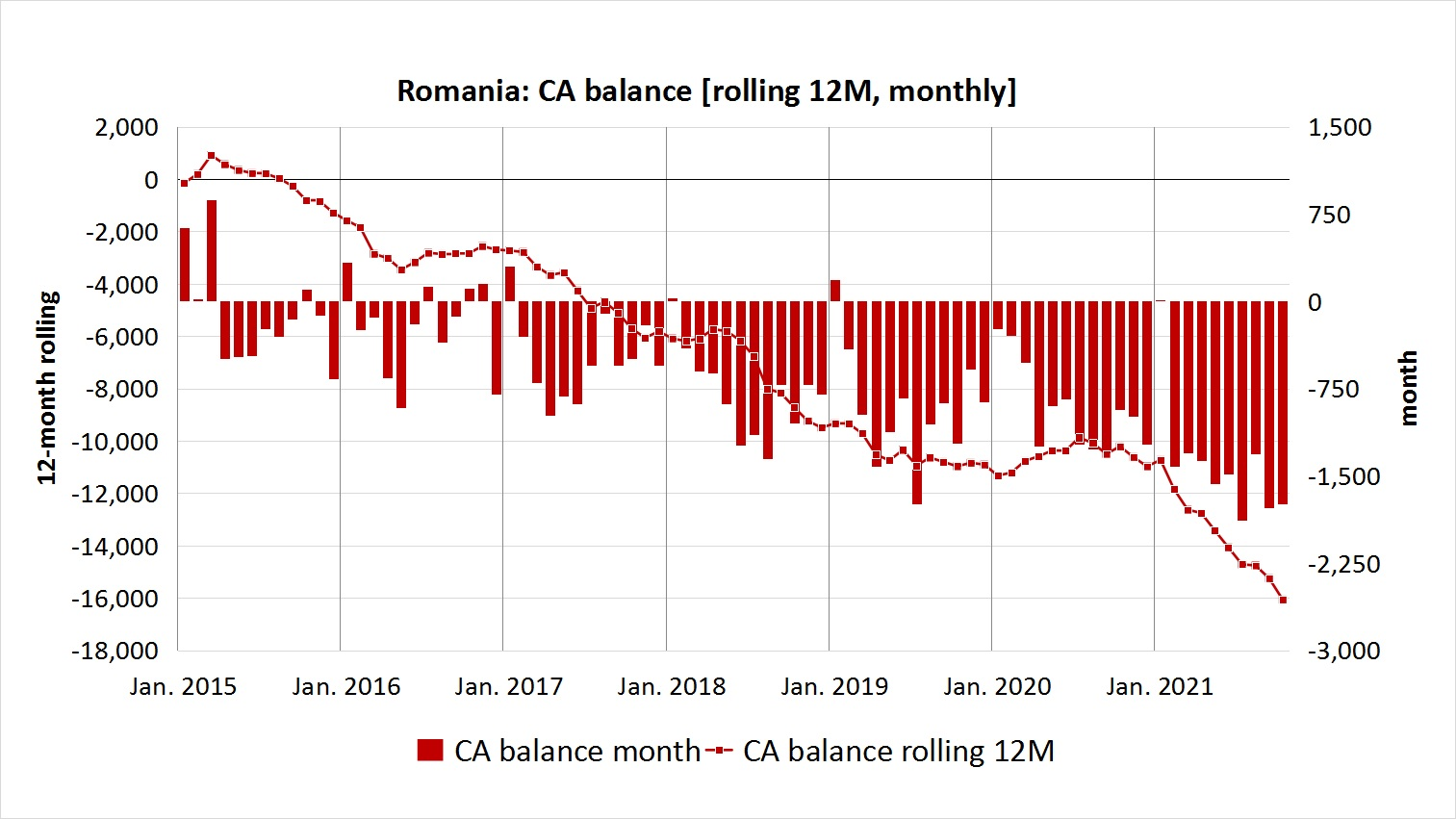

External environment: Romania’s current account deficit in the 12-month period to October 2021 widened by 57% y/y, reversing a small 7% y/y contraction posted for the comparable period to October 2020.

Overall, the country’s external deficit in the 12-month period to October deepened by 46% compared to two years earlier (taken as a benchmark for avoiding COVID-19 base effects), to €16.0bn.

The current account deficit-to-GDP ratio thus hit 6.9% in the 12-month period, sharply up from 4.7% in the 12 months to October 2020 and 5.0% in the period to October 2019. This is above the EC’s forecast for a 6.5%-of-GDP current account gap in 2021, followed by 6.3% in 2022 and 6.1% in 2023. The Romanian authorities are slightly more optimistic. Notably, most of the money under the Resilience Facility will enter the capital account of the balance of payments, thus financing the current account gap that is likely to remain wide over the period of implementation of the European Union’s programme.

The deficit of the trade with goods was the main element of the current account balance and it hit €22.3bn or a 9.5% of the GDP deficit in the 12-month period to October – up from 8.6% in October 2020 and 8.0% in October 2019.

The current account deficit had continued to expand at a very fast pace, adding more than 85% in 2021 H1 overall, versus the same year-earlier period, the minutes from the National Bank of Romania (BNR) October monetary policy board meeting read. The developments were viewed as particularly worrisome by board members amid a significant drop in the coverage of the current account deficit by autonomous capital flows in Q2, yet from a considerably higher level in the first month of the year.

Inflation and monetary policy: Romania’s headline inflation is expected to have hit 7.5% y/y at the end of 2021 to rise to 8.6% y/y at the end of the second quarter of 2022 as the temporary energy bill subsidies are phased out, and ease to 5.9% y/y at the end of 2022, under the revised inflation outlook revealed by the BNR on November 11.

Romania’s consumer prices continued to increase in December when the inflation reached new records, after prices remained constant in November, partly thanks to a subsidy scheme enforced by the government to moderate the energy prices.

Consumer prices advanced by 0.7% in December, driven by the electricity price that increased by 3.9% and contributed nearly 0.3 percentage points (pp) alone to the monthly inflation, according to data released by the statistics office, INS.

The annual inflation reached 8.2% y/y and energy prices in general (electricity, natural gas, heating and fuels included) contributed more than half, more precisely 4.3 pp.

The BNR increased the refinancing rate by 25bp to 1.75% on November 9, against consensus expectations for a steeper tightening of the monetary stance.

However, it also widened the symmetric interest rates corridor, consequently raising the Lombard rate by 50bp to 2.5%, which is likely to have a visible impact on the money market rates, while keeping the deposit facility rate at 1%.

This was followed by a more modest increase in the refinancing rate by 25bp to 2.00% at the bank's January 10 monetary board meeting, when it also widened the interest rate corridor by another 25bp to 1pp. The 25bp rate increase was smaller than bank analysts anticipated, and left Romania with the lowest refinancing rate among its peers as of January 2022.

Given that it acted too little, too late, Romania’s central bank will have to increase its refinancing rate not only in 2022 but also in 2023, taking it up to 5.5%, according to a research report by JP Morgan.

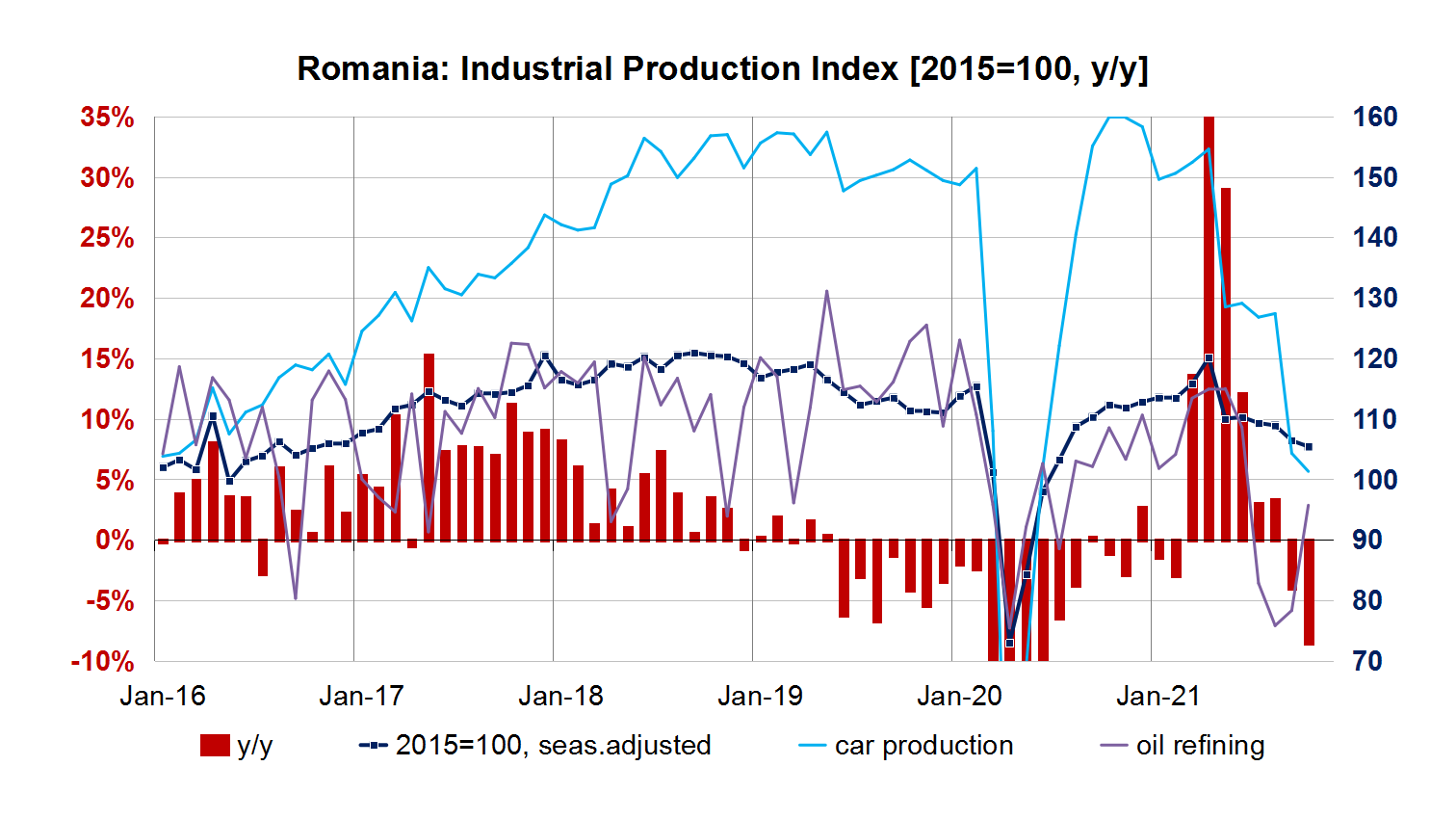

Industrial production: Romania’s industrial production declined again in April-October 2021 after a brief post-COVID recovery, while the outlook for 2022 remains uncertain.

The country’s industrial output had been dwindling before the crisis, but that was seen at that time as a sign of consolidation toward more value-added and highly productive segments, forced by tight labour markets. At this time, however, the slowdown simply reflects disruptions across the global production chains that are particularly visible in the automobile industry. High energy prices have also forced some industries (such as fertiliser and automotive production) to reduce operations. In Romania, an accident at the biggest refinery, Petromidia, also impacted the overall industrial output.

As of October 2021, the 12-month industrial output increased by 6.8% y/y, after a 9.9% y/y contraction posted in October 2020. The seasonally-adjusted industrial output in October 2021 was in the region of the values seen in 2017.

Real economy

Retail: Romania’s retail sales index contracted in October 2021 compared to August by 4.8% in absolute terms and by 1.0% in seasonally adjusted terms, reversing the gain accumulated in May-August.

The annual growth rate of the retail sales volume eased to 4.0% y/y in October from 6.8% y/y in September.

Compared to October 2019 (before COVID-19), the retail sales index in October 2021 was higher by 8.1%, or 4.0% in annualised terms.

In annualised terms compared to October 2019, food sales rose moderately by 3.7%, sales of non-food goods surged visibly faster by 8.4% and fuel sales contracted by 3.3% under direct and indirect mobility constraints.

As regards post-lockdown developments, retail sales recovered robustly from the weak performances during the first stages of the pandemic until May this year.

The propensity for consumption was meanwhile depressed by a multitude of factors including slower nominal wage growth, rising inflation, negative expectations particularly in regard to energy prices and interest rates.

The outlook was complicated once the new variant of COVID-19 generated more caution as regards 2022, previously seen as the year of recovery.

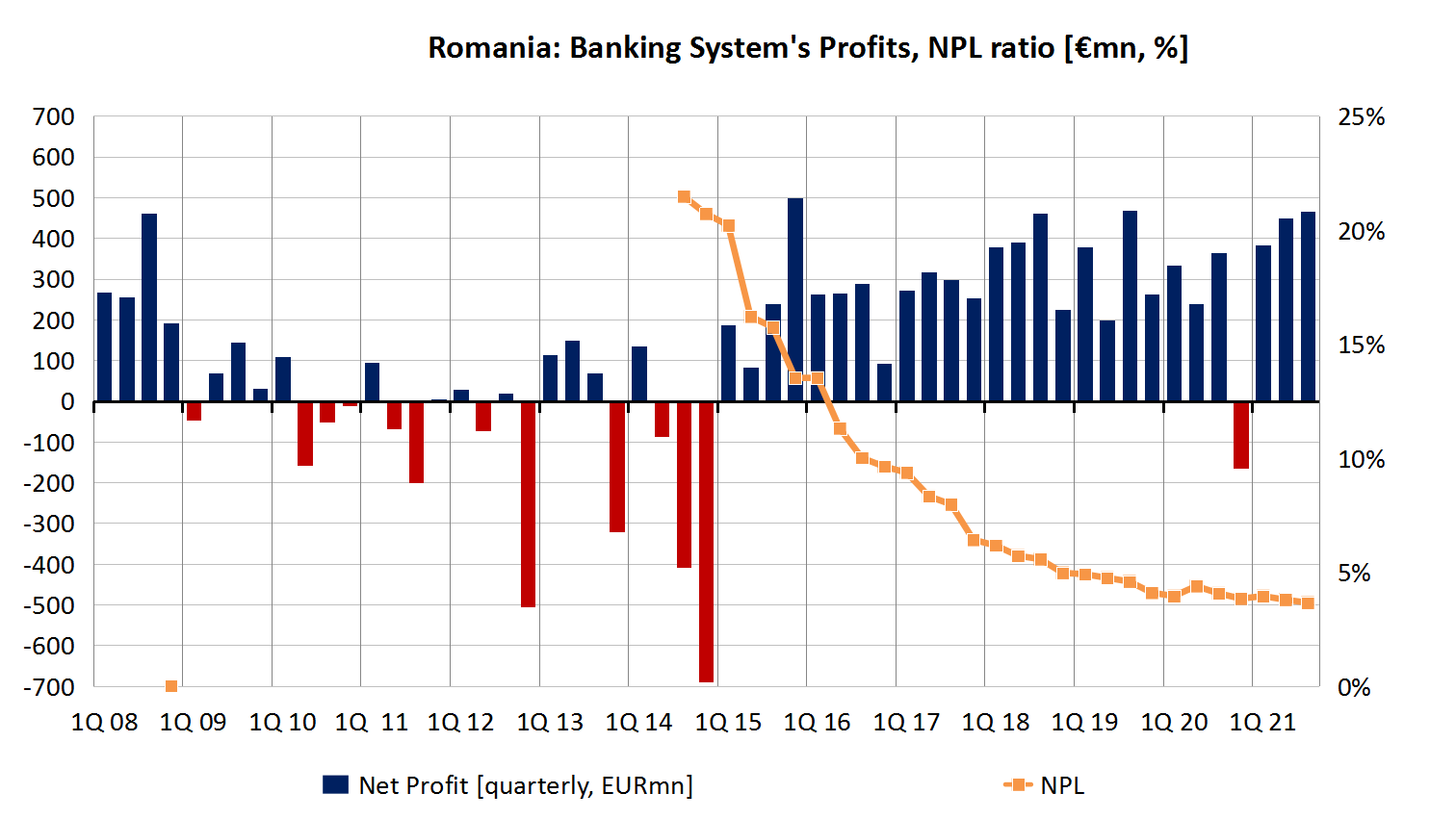

Banks: Romanian banks came out of the crisis in better shape than they entered it.

The Romanian banking system posted RON6.4bn (€1.3bn) aggregated net profit in January-September 2021, 37% more than in the same period of 2020 and 24% more compared to the same period of 2019, according to data released by the BNR.

Banks’ non-performing loan (NPL) ratios were also decreasing.

The ongoing rise in interest rates bodes well for the banks’ profits, but not necessarily for the quality of their portfolio loans (or for their debtors’ balances).

The banking system’s NPL ratio dropped to 3.7% at the end of September 2021 from 4.1% one year earlier and 4.4% in mid-2020 during the climax of the crisis.

The net assets of the banking system rose by 13% y/y to RON603bn at the end of September 2021, roughly in line with the rise in the non-government loans portfolio (RON315bn, +13.4% y/y). The volume of government loans surged by 21% y/y to RON163bn at the end of September 2021.

Some sectors of Romania’s economy may have faced problems during the COVID-19 crisis, such as hotels, restaurants and cafes (HoReCa) or more recently the automobile industry, and the economy as a whole has lost steam after recovering from the lockdown quarter — but this has nothing to do with the banking system that is now faring better than ever.

Industry: After a full post-COVID recovery, Romania’s industry returned to the downward trend that prevailed before the crisis.

Romania’s seasonally adjusted production index decreased in October 2021 by 0.9% m/m (-1.7% m/m for the core manufacturing industries) compared to September, marking the fourth consecutive month of negative performances.

The annual change in the index is less relevant, given the base effects, but the seasonally adjusted index reveals a visible industrial slowdown since March-April this year.

The automobile industry and oil refining (due to the accident at the Petromidia refinery) were mainly responsible for the decline. The former delivered in October an output that was 33% inferior to that delivered in October 2019 (before the crisis), while the two-year contraction in the case of the latter was 20%.

Overall, for the whole industry (mining and utilities included) the decline compared to October 2019 was 9.6% (-4.9% per annum) and for the manufacturing sector, it was 13% (-6.7% per annum).

In October 2021, industrial activity was dragged down by the automobile industry (-3.0% m/m) that has particularly underperformed recently due to the semiconductors crisis, but also by other industries such as pharma production (-13.2% m/m).

In contrast, the oil refining industry recovered for the second month in a row after Rompetrol’s Petromidia refinery resumed operations at the end of September.

Energy & power: Romania’s energy market has a robust outlook and projects are being drafted to address the rising energy prices and scarcity — but regulation of the sector is key for unleashing its robust potential.

Local problems in Romania added to the tense situation of the European energy markets in 2021. Both households and corporate consumers were impacted by rising prices. Residential electricity market liberalisation, effects of accelerated decarbonisation (rising price of CO2 certificates) and supply disruptions across the whole of Europe overlapped and resulted in record prices. The government set in place a “cap and subsidy” mechanism aimed at protecting households, particularly low-income ones, while prompting concerns among energy producers and suppliers.

One of the key issues that became visible in 2021 is the insufficient power generation capacity. Natural gas self-sufficiency (over 90% in recent years) dropped as well. Furthermore, Romania agreed to phase out the use of coal by 2032, under the Resilience Plan.

To address these, Romania must pursue the projects already outlined in the nuclear, renewables and natural gas sectors. Bolstering nuclear power capacities with two more traditional reactors and new, small-sized reactors planned with US partner Nuscale is part of the answer. Construction of new wave of wind and PV generation capacities is taking place. But the offshore wind segment needs legal clarifications. The natural gas producers, including OMV petrom, Romgaz, BSOG and Lukoil, are waiting for a new Offshore Law for starting production.

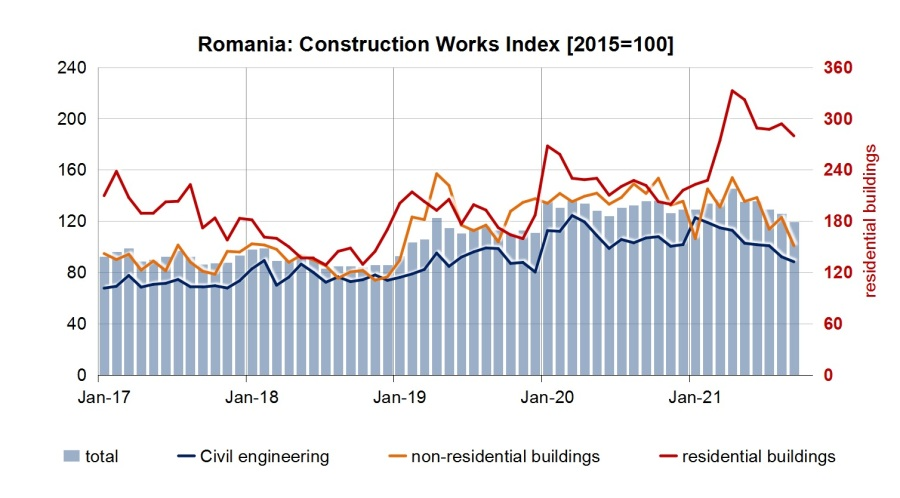

Construction: After outstanding performance during the COVID-19 year 2020, Romania’s construction sector shows signs of fatigue. But the Resilience Plan is likely to provide fresh impetus after 2022.

Romania’s construction sector has constantly lost ground since April 2021, and it marked a significant 7.5% y/y decline in Q, 2021.

However, the sector demonstrated outstanding resilience during the crisis in 2020, which is why it isn’t now enjoying the benefits of low base effects seen in other industries and more broadly in terms of economic growth.

The trend has been visible in all three market segments: residential buildings, non-residential buildings and civil engineering.

However, the residential buildings sector made a substantial 29% y/y annual advance while the non-residential buildings (-22% y/y) and civil engineering (-13% y/y) posted negative annual performances.

In response to the unexpected negative developments in the construction sector, the state strategy and forecasting body, CNSP, abruptly revised downward its forecast for the value-added generated by the sector this year to a dismal 0.2%, from 6.1% envisaged in August.

Part of the revision may be attributed to the rise in the price of construction materials and energy.

The sector is expected to recover in 2022 when the value-added generated by construction companies is set to surge by 9%, driven by the much-expected projects financed under the Recovery and Resilience Programme.

Major sectors: November 2021 brought some good news for Romania’s automobile industry, but there’s no sustainable recovery and furthermore the overall mood remains negative due to the industrial slowdown across the whole of Europe.

The number of cars produced in Romania has more than doubled in November compared to October, according to the industry association ACAROM. Both Romanian producers, Dacia and Ford, delivered 46,773 units in November compared to 18,277 units in October.

Ford even managed to surpass its output of November 2020, as it recovered fast from the subdued activity in October.

In the first 11 months of 2021, Romania produced 379,952 cars, 6.1% down compared to the same period in 2020. The decline was smaller for Dacia, which produced 233,984 cars, 2.6% fewer than last year. At Ford, the 11-month production shrank by 11.2% due to repeated shutdowns, to 145,968 units.

Budget and debt

Romania’s general government budget will still stand at 6.3% of GDP in 2023, double the 3% threshold it has to drop under by 2024, according to the European Commission’s Autumn Forecast published on November 11.

The country’s general government budget’s deficit will shrink by 1.4pp from 9.4% of GDP in 2020 to 8% of GDP in 2021 (on one-off elements) but the fiscal consolidation will measure only 1.7pp over the coming two years — leaving the public deficit at 6.3% of GDP in 2023, according to the forecast.

Under the Convergence Programme and Excessive Deficit Procedure, the country's public deficit should be brought under 3% of GDP by 2024.

Romania’s new government, headed by Liberal Prime Minister Nicolae Ciuca but controlled by the Social Democrats, announced plans to finish drafting the 2022 budget by the end of 2021.

The deficit target will be maintained in line with the agreements reached with the European Commission: 5.84% of GDP in cash terms and 6.3% on an accrual basis (ESA methodology), sources said.

The government has reportedly drafted nine bills to increase tax collection.

As regards investments, the 7%-of-GDP minimum level previously announced by the Liberals will be observed as well.

However, only mature projects will be financed from Resilience Facility money in order to avoid having to return the money because of delays in the implementation of the projects.

Romania’s public debt to GDP ratio edged up by only 1.1pp in January-September 2021.

Romania’s public debt rose by €9.8bn including the exchange rate effects in the first nine months of 2021 to RON556.4bn (€112.5bn) at the end of September, the Ministry of Finance announced on December 8.

The debt-to-GDP ratio edged up by only 1.1pp from 47.4% at the end of 2020.

The wide deficit planned by the government for Q4, however, will bring the debt to GDP ratio close to 50% again.

As the new ruling coalition promises to stick with a cash deficit target of 5.84% of GDP in 2022 and the nominal GDP will rise, the indebtedness as reflected by the debt to GDP ratio would not rise much over 50% at the end of next year.

Moody's projects Romania’s debt-to-GDP ratio will continue to rise in 2022 and 2023, and peak in 2024 at 56.6% (gross terms) before starting to decline in 2025.

Under a more optimistic scenario (not far from the government’s plans) Standard & Poor’s projects a milder trajectory of the public debt to GDP ratio, seen as remaining below 50% in net terms by the end of the forecast period (48.1% in 2024, after peaking at 48.6% in 2023) and not much above 50% in gross terms (52.4% in 2023 and 51.6% in 2024).

Markets

The Bucharest Stock Exchange’s (BVB's) flagship index, BET, closed the trading session on December 28, above 13,000 points for the first time since its launch in September 1997.

The BET, which follows the evolution of the most traded 19 stocks on the BVB, gained almost 33% during 2021, which makes it one of Europe’s top 10 best-performing country indices in the year , according to Trading Economics data.

Three companies that are part of the BET index have seen their shares go up more than 100% in the last year: construction materials producer Teraplast (+195%), nuclear power producer Nuclearelectrica (+165%) and medical services provider Medlife (+135%).

Energy groups OMV Petrom (SNP) and Romgaz (SNG) and investment fund Fondul Proprietatea (FP) also recorded above-average performances of 35-38% in the last year.

At the opposite end, aluminium producer Alro (ALR) was the BET’s poorest performer in 2021 with a drop of almost 20%. Utility companies Transgaz, Transelectrica and Electrica also recorded double-digit losses.

Including the dividends, investors obtained a yield of 40%, reflected by the dynamics of the BET-TR index.

All stock market indices increased in 2021, the individual gain ranging from 21.1% for BET-FI, the index that tracks the performance of SIFs (closed-end investment funds) and Fondul Proprietatea (FP), to 40% for BET-TR, the index that includes the dividends granted to shareholders.

Last year, the stock market operator also launched the BETAeRO index for the secondary trading market AeRO, which ended the year with an appreciation of 5.3% compared to its launch on October 11.

The capitalisation of the main segment rose by 48.4% in 2021, to RON229bn (€46bn), while the capitalisation of the secondary segment AeRO increased by 103.3%, meaning it doubled to RON19.8bn (€4bn).

_1752202224.jpg)